The Ultimate Guide for a First-Time Home Buyer - The Home Buying Process in the city of Los Angeles County.

Most people have trouble when buying their first home, especially, if they’re opting for a mortgage loan or some other form of lending. Besides, buying a house is a one-time investment for most people. Therefore, ignoring any important step or requirement can lead to an expensive mistake in the long run.

Let's go over the entire home-buying process in Los Angeles County. Overall, this guide will encourage you to find the best suitable home and make the right purchase by adhering to all the valid principles of home buying in Los Angeles County.

Please see below The Times’ neighborhood map of Los Angeles County. This regional view is your portal to individual maps and statistics for 158 cities and unincorporated places and 114 neighborhoods within the city of Los Angeles. In addition, there are maps of 42 unincorporated areas that we have collapsed inside of adjacent cities. The maps cover the 4,000 square miles of Los Angeles County — by far the most populous county in the nation — from the high desert to the coast. In 2009, there were an estimated 9.8 million residents, up from 9.5 million counted in the 2000 U.S. census, the basis for The Times’ demographic analysis for each neighborhood and region.

Los Angeles is a sprawling Southern California city and the center of the nation’s film and television industry. Near its iconic Hollywood sign, studios such as Paramount Pictures, Universal and Warner Brothers offer behind-the-scenes tours. On Hollywood Boulevard, TCL Chinese Theatre displays celebrities’ hand- and footprints, the Walk of Fame honors thousands of luminaries and vendors sell maps to stars’ homes. Area: 503 mi² ― Source: Google

Santa Monica

First-Time Home Buying Process

Let’s suppose you have saved up enough money and maintained a reliable credit score to qualify for a home loan. You might wish to make a down payment right away once you come across the house of your dreams. But we suggest that before doing that, you should make sure of a few things. And, one of those things is the home buying process. Learning the process early, i.e., before the real estate transaction begins, will help you determine which tasks require your maximum attention and which don’t.

The pain and havoc that certain unfamiliar processes and steps create can baffle most first-time home buyers. There are offers, counteroffers, furious negotiation, paperwork duties, and a lot more that lead to a complete home purchase. Here’s what you can expect when you try to navigate through the real estate market.

Search for a Home in Los Angeles

One of the main things that lead to discrepancies is that certain homebuyers stick to a single option, while the real estate market remains flooded with various open-for-sale listings. Working with a knowledgeable real estate agent is the key.

Of course, you should carry out your own research by reading the newspaper, exploring the internet, inquiring among friends and family, and searching through local house listings. Download Los Angeles Home Search app to see listings.

The first step of the home buying process is making up your mind about a property.

You should proceed by making an offer only if you think that a property is suitable to accommodate you and your family for the period that you wish.

It might sound like a cumbersome task, but you should never forget that there are plenty of houses that are not only listed for sale but also extremely feasible against their asked prices. Note that you shouldn’t walk into a serious real estate transaction without a reliable realtor or real estate agent by your side. Furthermore, you should ignore certain imperfections inside or outside the house if you are low on budget and you think that your chosen home has incredible potential in terms of resale value.

Consider Your Finance Options

Once you contact a reliable real estate agent in your locality who is aware of all the real estate codes, rules, and regulations, you can discuss your options with them. On top of that, make sure that you consider all the properties that coincide with your residential interests.

Once you set your sights on a specific property, you should proceed by considering all the finance options you have. This step is not for people who have enough savings to pay for the home upfront, cash buyers. If you are not a cash buyer, let's look through various house loans and mortgage plans.

Some mortgage loans, especially those for novice homebuyers, only require a 2-3 percent down payment. In reality, you may also come across certain mortgages and house loans that don’t require a down payment at all. However, in such cases, the high interest rates might put you off, so it is best to go with plans that require a certain proportion of the loan’s value as a down payment.

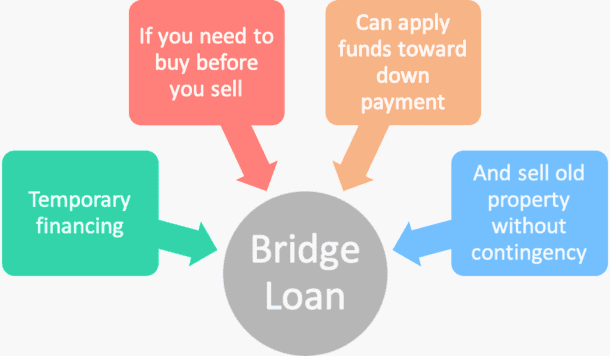

Bridge Loan

A bridge loan is a short-term loan used until a person or company secures permanent financing or removes an existing obligation. Bridge loans are short term, up to one year, have relatively high interest rates, and are usually backed by some form of collateral, such as real estate or inventory. The rate depends upon the loan amount and capacity to repay. Until a permanent source of funding is generated, the loan bridges the gap between two consecutive funding periods. The loan gives borrowers access to a short-term loan, enabling quick liquidity i.e. cash in hand to fulfill the current obligations. The loan term ranges from 2-3 weeks and can extend up to 12 months.

A simple solution to bridge the gap between the home you have and the home you want.

Compass Bridge Loan Services provides access to competitive rates and dedicated support from well established industry lenders, with the exclusive option to get up to six months of your bridge loan payments fronted when you sell your home with a Compass agent.

Bridge Loan Advance

Work with a Compass agent to sell your current home and get up to six months of your bridge loan payments and other associated costs fronted — an exclusive offering for Compass clients, regardless of the lender you use.*

Is your money tied up in the equity of your current home?

If you want to move but your money is tied up in the equity of your current house, a bridge loan can help you secure funding to facilitate the transition to a new home — like for a down payment or mortgage payments. Once your current home sells, you can use the proceeds to pay the bridge loan back.

Who is eligible for the Bridge Loan Advance?

The Bridge Loan Advance is available exclusively for qualified clients with a traditional bridge loan who are working with a Compass agent to sell their existing primary residence.*

Do you need to move within a specific timeframe?

If you're relocating for a new job or other reason, a bridge loan can afford you the freedom to move on your own terms and secure a new house when you need to, without having to wait for your old home to sell.

Does your home require renovations or other work?

Whether you're using Compass Concierge to increase your home's value, or are making improvements on your own, it may be easier to have construction work done when you're out of the house. A bridge loan can help you move faster so you're out of the house while those improvements are being completed.

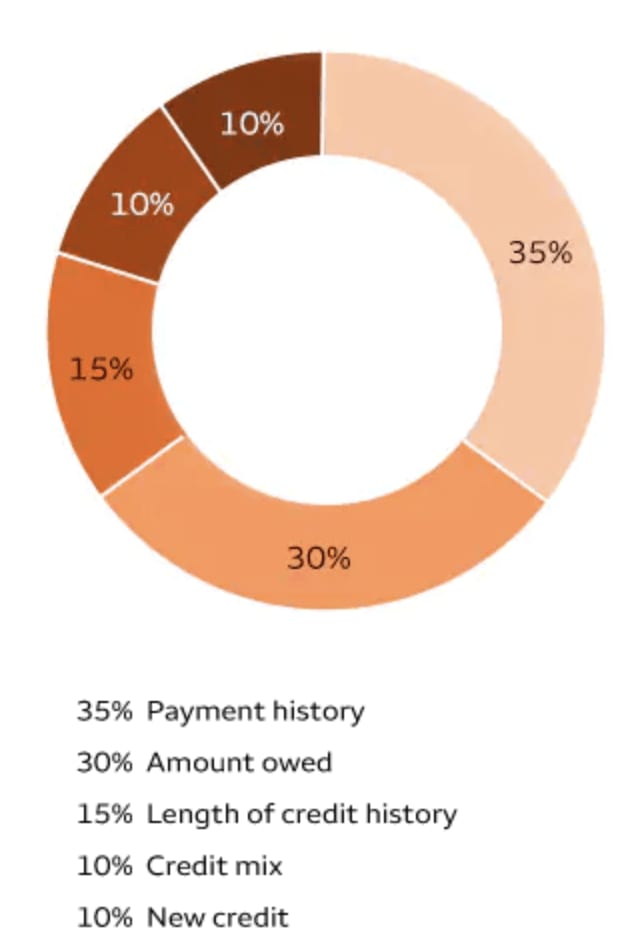

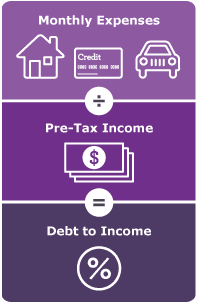

Following the selection of a lender, you will go through the verification process. This process will require all your valid, authentic, and latest financial information to confirm your banking interests. Some of the required key information will include employment status, credit scores, your debt-to-income ratio, etc. Your credit score is one of the most important measures of your creditworthiness. For your FICO® Credit Score, it's a three digit number usually ranging between 300 to 850 and is based on metrics developed by Fair Isaac Corporation. The higher your score is, the less risky you are to lenders. By understanding what impacts your credit score, you can take steps to improve it. See the five pieces of your credit score here.

Your debt-to-income ratio (DTI) compares how much you owe each month to how much you earn. Specifically, it’s the percentage of your gross monthly income (before taxes) that goes towards payments for rent, mortgage, credit cards, or other debt. To calculate your debt-to-income ratio, click here.

The lower the DTI; the less risky you are to lenders.

Offer a Price for the Home

After discussing with your real estate agent in detail, both of you will make an offer to the selling party. Once your agent offers a price for the home, the seller’s agent will either produce a counteroffer or accept your offer. But, when counteroffers start flying, the negotiation begins and it might take a certain amount of time before the parties settle on a price.

After finalization of the price, make sure that you consider the closing costs that will slightly raise the overall property purchase cost. The closing costs could include any walk-in appliances, repairs, minor renovations, commuting costs, etc. As a suggestion, try to get the past 12 months’ utility bills to get an idea about the average living costs beforehand.

After reaching a consensus, the deal settles and the price’s decided. You will deposit earnest money (good-faith deposit usually 3%) to move the process towards an escrow. The Escrow Holder must provide an accounting of where the money deposited by Buyer and his Lender went. The Escrow Holder collects the Buyer's downpayment and the Lender's loan funds. At the closing, using all funds collected, the Escrow Holder pays the Seller's loans, liens, and Vendor bills approved by parties.

In Los Angeles County, California, as in many states, the real estate escrow process can take around 30 to 40 days on average. It can go longer in the case of a more complicated transaction. It can also happen faster, if everything goes smoothly and there are no backlogs. During an escrow the property comes off the open market listing and lets you conduct on-site inspections.

Get a Home Inspection and an Appraisal

Unless you plan on paying all cash for your new property, you will likely need a home appraisal in California. Your lender will order your appraisal on your behalf, and there are several basic types of appraisals including Desk, Exterior-Only, and Full Inspection.

Appraisal Waivers or “Property Inspection Waivers (PIWs)” allow borrowers and lenders to skip the home appraisal process entirely in California when buying a home. There are, however, very strict criteria that must be met before a PIW is granted. PIW requirements discussed in this short blog from https://www.jvmlending.com/ but the basic requirements are below.

Your realtor can recommend a home inspector. A buyer hires and pays a home inspector to inspect every aspect of the house that falls under their duty. Home inspection deal-breakers are quite important so pay attention to what your home inspector reveals to you about the house’s overall condition. Conclusively, many homebuyers like to have a home appraisal to determine the fair market value of the house that they have decided to purchase.

Close the Deal – Or Look Elsewhere

Once the process is complete and everything is in order, you will sign extensive paperwork to finally the ownership will be transferred from the seller to your name.

f you just bought the home, your mortgage will be on the title as a lien.

You will then fund the seller, get a deed, which is a document you get at closing that states you own the property. A deed is an official written document declaring a person's legal ownership of a property. You become a homeowner and get a key to your property.

Conclusion

Now that you are aware of the most important details of the home buying process in Los Angeles County, remember that a real estate agent, home inspector, and home appraiser aren’t the only people that you need. You might require the guidance of a real estate attorney at your side to help you avoid any legal issues or problems during a real estate property purchase.

Reference/Source:

httpss://Compass.com

https://www.discover.com/home-loans/articles/10-steps-to-buying-a-home/

https://www.bankofamerica.com/mortgage/first-time-home-buyer/

https://www.nerdwallet.com/article/mortgages/home-buying-checklist-steps-to-buying-house

https://www.usbank.com/home-loans/mortgage/first-time-home-buyers.html

https://www.nytimes.com/guides/realestate/how-to-buy-a-house