In the aftermath of this devastating event in Los Angeles, Compass wants to provide clear and supportive guidance to help begin the recovery process. Please share the following with whomever may need it. Please review the following steps to prioritize your safety and secure the necessary assistance:

Immediate Actions

Contact Your Insurance Provider:

• Initiate your claim as soon as possible.

Register for Assistance:

• Sign up with FEMA and the American Red Cross

for immediate support and resources.

Documenting Losses for Insurance

Create a List of Lost Items:

• Start an itemized list of your belongings while it’s

fresh in your mind.

• Go room by room mentally and write down major

items. Details can be filled in later.

• Keep a notepad with you to jot down items as you

remember them.

• Photos can help jog your memory but only use

them if it’s not too upsetting.

Download a free home inventory guide from the Department website, or receive a hard copy by calling the Department of Insurance Consumer Hotline at 800-927-4357.

Temporary Housing Assistance

Take Charge of Housing Solutions:

• Your insurance company will offer housing

assistance, but they may not fully understand

California’s competitive rental market.

• If you find a rental, provide your Additional Living

Expenses (ALE) representative with the contact

information so they can handle the arrangements.

• Even if you stay with family or friends, ALE can

reimburse them for the rooms you use.

Financial Documentation

Save All Receipts:

• Keep receipts for hotel stays, meals, purchases,

and any travel related to regular activities.

• Mileage driven for essential errands may also

be reimbursed.

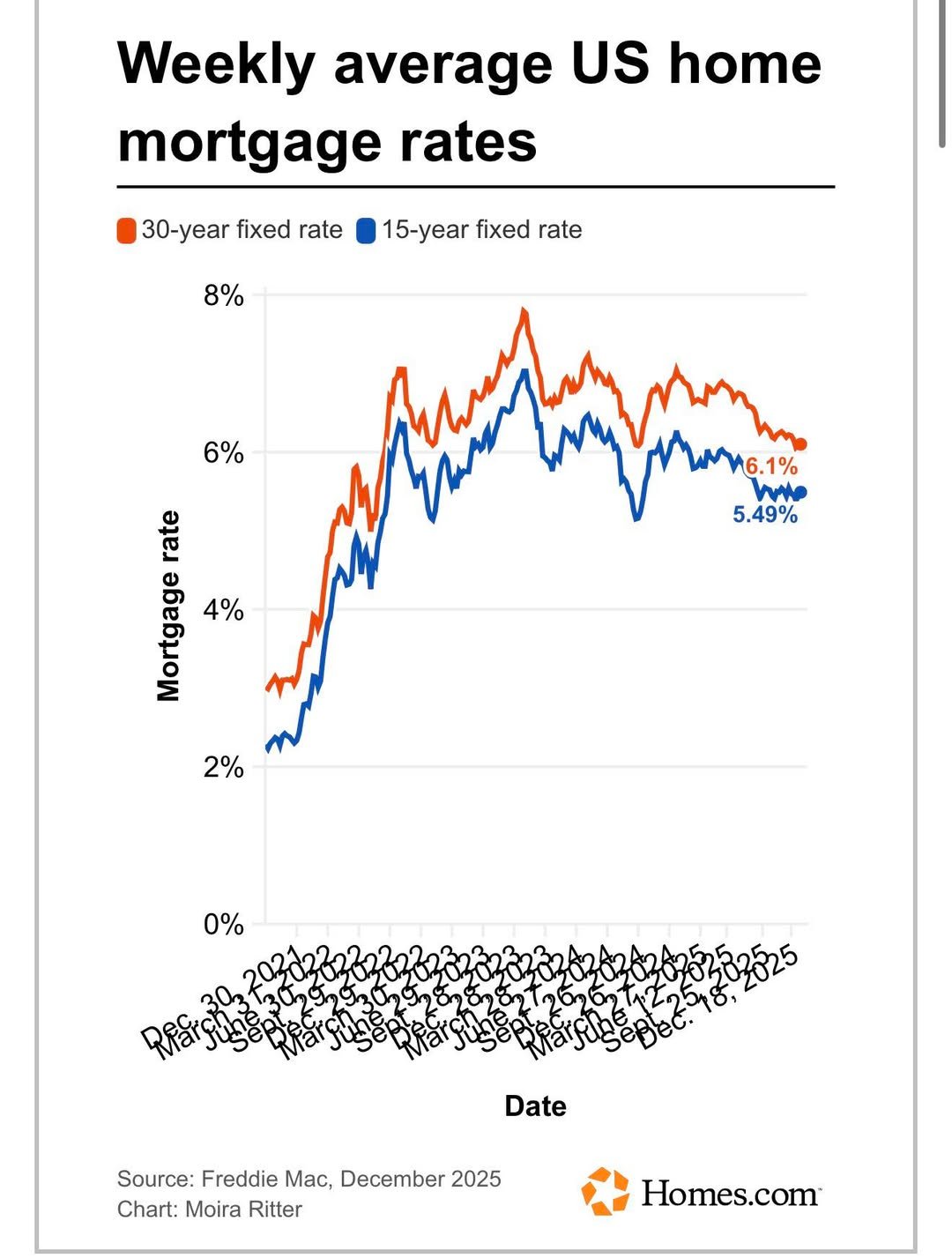

Homeowners usually have the option to pause mortgage payments for as much as a year if they are impacted by a natural disaster. This is called forbearance. Mortgage companies are required to offer it on the roughly 40% of loans backed by Fannie Mae and Freddie Mac. Loans backed by the Federal Housing Administration and the Department of Veterans Affairs have similar guidance. Forbearance is often doled out in three- or six-month increments. (WSJ)

Temporary Furnishings

& Household Items

Leverage Insurance for Household Needs:

• Your insurance can cover the rental of furniture,

mattresses, bedding, kitchen essentials, and basic

household items (vacuums, towels, trash cans, etc.).

• If you haven’t received donated items, rent what

you need for now—you can replace them over time.

Recovering Essential Documents

Visit the Local Assistance Center (LAC):

• Replace important documents such as your driver’s

license, birth certificates, Social Security cards,

passports, and vehicle registration.

• Explore every table at the LAC to close utility

accounts and access gift cards or support from

various organizations.

Emotional Well-being

Be Kind to Yourself:

• Experiencing forgetfulness and feeling overwhelmed

is normal. Be kind and patient with yourself during this

time. Natural disasters impact more than just physical

property—they can also affect mental health.

• The L.A. County Department of Mental Health is

offering support through its disaster distress helpline

(800-985-5990) or by texting the phrase “TalkWithUs”

to 66746.

• Residents can also try the department’s access line:

800-854-7771.

Attorney General Bonta urges Californians to

beware of fraudsters who may attempt to

take advantage during this natural disaster.

If it sounds too good to be true, it may be.

Do your research, and see the following tips

to protect yourself from scams:

Verify Credentials: Always check licenses,

certifications, and reviews for contractors,

adjusters, and charities. To find licensed

contractors check with the

Be Skeptical of Upfront Payments: Avoid

paying large sums upfront for services or

promises of assistance.

Confirm Authenticity: Use official

channels to verify government

representatives or relief efforts.

Monitor Your Accounts: Regularly review

financial accounts and credit reports for

suspicious activity.

Report Fraud: Report suspected scams

to local law enforcement or to his office

at Source:

Contractors State License Board oag.ca.gov/report.

https:/ www.oag.ca.gov/news/press-releases/attorney-general-bonta-local-leaders-share-tips-keep-californians-

safe-fires

TIPS FOR WILDFIRE CLAIMANTS

Obtain a complete copy of your residential homeowner's insurance

policy, including your declarations page. The law requires your

insurance company to provide this to you free of charge within 30 days

of your request. Ask your agent or insurer representative to explain how

much coverage you have (1) to rebuild or repair your home, (2) for your

personal belongings, and (3) for living expenses. This should include an

explanation of Extended Replacement Cost and Building Code

Upgrade coverages if applicable. Ask how to most effectively claim

your coverage benefits.

Take note of your Additional Living Expense (ALE) limits and manage

your ALE expenses in recognition of a long rebuilding process. Your

time to collect ALE after a declared catastrophe is no less than 24

months even if your policy says otherwise; however your amount of

coverage is not increased. An extension of up to 12 additional months,

for a total of 36 months, should be granted if you encounter delays

beyond your reasonable control.

Track all of your additional expenses that arise from having to live in

another location away from your home. Note: your ALE reimbursement

may be offset by your normal cost of living before the fire (i.e., ALE

does not pay for your mortgage or expenses you would normally incur)

but you are entitled to the same standard of living you had before the

fire. ALE will pay for temporary rent, additional mileage, etc.

Document all of your conversations with your insurer/adjuster about

your claim and policy limitations in a dedicated "claim diary." If your

adjuster says something is excluded, limited, or subject to certain

conditions, ask the adjuster to point out the specific provision in your

policy being cited.

Get at least one licensed contractor's estimate or bid on the cost to

rebuild your home just to get a reasonable sense of the actual cost as

compared to your coverage limits (for more considerations on

contractors, view the CDI's electronic brochure

and check the website.) While your insurance company may provide its own estimate, it may contain errors

or fail to reflect local conditions or demand surge. Demand surge

reflects price increases following a major disaster when contractors and

materials are in short supply.

Call the Department of Insurance Hotline for help at (800) 927-4357.

You can also . Consider insights from consumer

advocates. Contact CSLB at 1-800-321-2752 to obtain a free copy of their publications.

Contact Alena Lehrer | Compass | DRE02120134